Red teaming the next ~5 years of carbon removal

Carbon removal has made huge progress over the past ~5 years. Demand has gone from ~$0 to several billion, there are now 100+ companies working across a range of carbon removal pathways, and governments are more engaged than ever. At the same time, it’s still far from inevitable that carbon removal gets to climate-relevant scale in the timeframe needed.

At the end of last year, the Frontier team got in a room to do our version of a red teaming exercise for carbon removal, focusing not on 2050 but on the next ~5 years. If carbon removal fails this decade, why will it fail? We came up with 50+ reasons. Below is not a comprehensive enumeration of these, but rather a summary of what we believe to be some of the most significant short-term risks to mitigate.

To be clear, we are very much still optimistic that these can be solved. But naming the problems increases the likelihood we (collectively) can actually solve them. The purpose of this short piece is to call attention to a few areas that are deserving of more of our collective attention and resources.

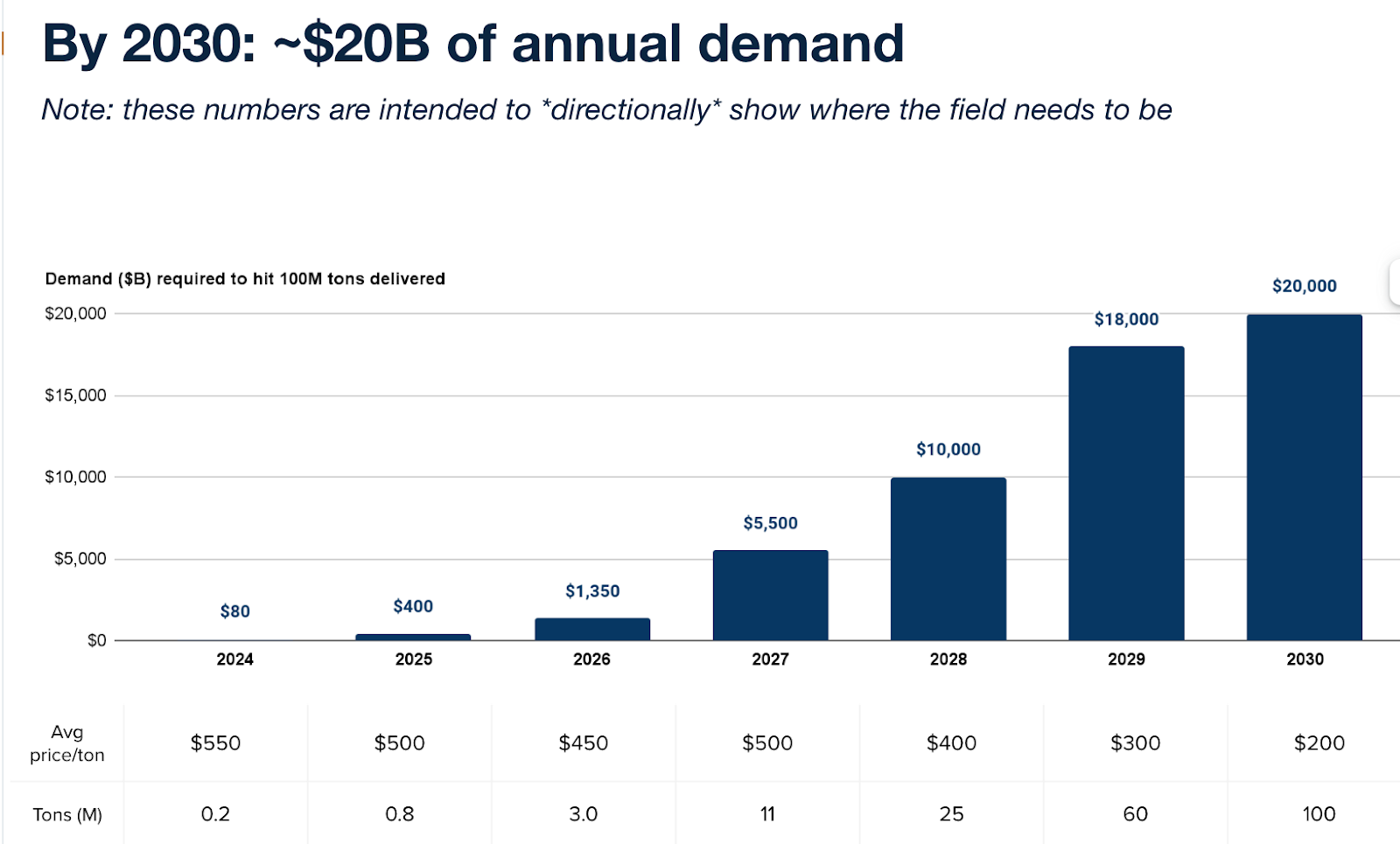

#1: Demand isn’t close to reaching the ~$20B needed globally *per year* by 2030 to meet science-based targets

Demand has grown massively in the past few years, but it’s not growing anywhere near fast enough to keep up with what IPCC models suggest we need.

The quick math: By 2050, the world will (very roughly) need ~$500B in annual demand (~5Gt at ~$100/ton). Even if we end up needing less and the price ends up being lower, the point is that the number is still very big.

To be generally on track for that, carbon removal needs to have scaled to ~50-100M tons per year by 2030. Let’s assume the average cost per ton in 2030 is $200, that’s ~$20B/year.

For context, Frontier is ~$1B over 8 years. Of course, there are other big buyers beyond Frontier (i.e. Microsoft). But the total demand that we are aware of comes nowhere close to what’s needed. And, to make matters more challenging, supply typically lags demand; carbon removal companies need offtakes now in order to build facilities that can deliver tons later.

So where might this demand come from?

(1) Policy-driven-demand: There is of course no question that policy is critical in driving long-term demand. But policy is also critical in creating the near-term demand, largely because the voluntary market is unlikely to make up much/most of the ~$20B/year by 2030. While innovative policy initiatives have dramatically accelerated in the past few years (i.e. the DOE’s procurement program and DAC hubs), the known list of global initiatives don’t add up to anywhere close to that $20B/year. We’ll need a portfolio of policies from many different countries to generate the demand needed. These initiatives will take time to get written/passed/implemented, so planting these seeds in the next few years is critical.

(2) Voluntary demand: Policy takes time. In the interim (especially in the next 2-5 years), we need many more voluntary buyers to fill the gap. Without near-term offtakers, many existing carbon removal companies are likely to stall out. To bridge the gap, we’ll need many more voluntary buyers supporting the most promising approaches.

What to do about it (in broad strokes):

Place *many* more policy bets across a broader set of geographies. The expected value of these global bets should stack up to ~$20B/year by 2030 (and continuing to ramp up after that). Getting more creative and proactive now is paramount.

Get SBTi to make carbon removal a part of their Net Zero standard. Many corporates have made voluntary net zero commitments via SBTi. However, today these standards don’t require or reward buying carbon removal as part of a corporate’s overall climate strategy. Without structural changes like this, voluntary dollars are unlikely to flow into early-stage carbon removal projects at anywhere near the rate needed.

Insetting from large industrials (mining, ag, etc.) is potentially a large, untapped source of demand that could be enabled through policy or voluntary standards. Industrials collectively own and operate assets that could generate huge volumes of carbon removal at relatively low cost.

#2: Even with fully signed offtakes, many companies are still having trouble accessing the capital needed to put steel in the ground

Even with fully signed offtakes, many CDR suppliers are still having trouble accessing the capital needed to build big new facilities, especially at reasonable cost of capital. The amounts they need are too big for venture, and too risky for traditional lenders who are unfamiliar with most CDR pathways. In some cases, the problem is accessing any financing at all. In some cases options are very high rates (e.g. 25%) and often include unfavorable covenants.

The net effect for suppliers is is some combination of (1) delayed timelines to build new capacity because raising capital takes a huge amount of time, (2) higher costs due to high cost of capital, or (3) projects just don’t happen at all.

What to do about it (in broad strokes): Find creative solutions that pull in concessionary capital to reduce risk for lenders while these technologies are in early stages.

#3: In the not-so-distant future, some pathways and companies will prove unviable or less attractive than initially thought. While this is normal and to be expected, it could threaten already tenuous demand.

Many carbon removal approaches are relatively early. We’re still learning whether an idea that sounds great in theory is actually great in practice. We should expect a number of companies, approaches—and even some pathways altogether—to fail. This isn’t because they weren’t good ideas, but rather because (1) ideas have to be tested in the real, physical world, and (2) most startups fail—building any company is hard, let alone a carbon removal company.

While failure—especially at this stage—is expected/normal, it’s possible that these failures get taken out of context, oversimplified by the media, and ultimately spook buyers, investors and policy experts (“carbon removal is too risky/will never work”).

What to do about it (in broad strokes): When these failures happen (they will—likely starting in the next few years), let’s do our best to (1) contextualize them and (2) extract the learnings to inform how to best help the field scale responsibly, and (3) be careful about making overarching claims about the entire field.

#4: There still probably aren’t enough ideas being tried, and there isn’t enough redundancy of the best ones.

If most startups fail, and the speed of scale-up demanded by IPCC models would be hard to achieve by an army of companies, let alone a small handful of them—are there enough world-class teams pursuing the most promising pathways? Our strong hunch is “no.”

Furthermore, despite a huge and recent diversification of carbon removal approaches being tried, we suspect that there are still many more great ideas that haven’t yet been tried. In the grand scheme, this field is still young and it’s probably too early to stop shaking the tree for ideas with differentiated cost and volume curves.

What to do about it (in broad strokes): If you’re excited about building a carbon removal company it’s not too late!

#5: Examples of other risks from our red teaming exercise that we’re tracking.

All the pathways are just less promising than we thought. Cost doesn’t come down, MRV is harder than expected, new regulatory/permit requirements balloon cost, and unknown-unknowns make all or most of the pathways less promising than anticipated in the long-run.

The permanent CDR market ends up fraudy/scammy and undifferentiated from low-quality offsets today. Low trust ultimately/eventually results in less demand.

The projects that get built aren’t wanted by the communities they’re built in, creating local and eventually political backlash.

Regarding Topic 4

Most funding audiences are afraid of speculation. The current focus for funding is to do something soon and tell a story about how cheap CO2 capture will be when carbon-free energy is plentiful. Earning revenue is the primary driver.

This funding process generally limits technology concepts to TRL 5 or better.

If the best CO2 capture technology has not yet entered the lab, then that technology has limited to no path forward. That technology will not participate in solving our excess atmospheric CO2 problem.

As long as funding audiences focus on cost and time ($100 per ton by 2030), the truth of CO2 capture (GJ/ton) will be limited to today's technology portfolio.

How does speculation get funded? I bet funding audiences will take more risk 10 years from now. But then it may be too late to be useful.

"Get SBTi to make carbon removal a part of their Net Zero standard" - I think the elephant in the room for me is that my understanding is that CDR is an eventual last resort for only the toughest to decarbonise sectors.

So while *some* CDR is needed in the future, there is definitely some element of fossil fuel companies using it as a political cover.

At the same time, I completely support industrial policies/voluntary standards that incorporate the cost of carbon (e.g. via CDR costs), and given how slow decarbonisation is going this could be a huge source of demand for CDR.